Typically, the summer months bring increased volatility and subpar returns for financial markets —but this year was an exception. Market conditions remained relatively stable, and both U.S. and international equities performed well. Global bond markets were generally quiet, with yields on U.S. government bonds moving slightly lower. As signs of labor market weakness emerged, the Federal Reserve shifted its focus toward supporting employment, even though inflation remains above the 2% target at 2.92%

In the U.S., the S&P 500 gained over 8% for the quarter, while international equities posted gains of nearly 10%. Domestically, technology and AI-related stocks continued to lead the charge. Overseas, performance was boosted by a rebound in Chinese equities and fiscal stimulus measures implemented by several European governments.

The continued rally in U.S. stocks has pushed the Shiller Cyclically Adjusted Price-to-Earnings (CAPE) ratio to its third-highest level in history. Historically, when the CAPE ratio has reached these levels, future returns have tended to be below average. However, earnings forecasts for 2026 and 2027 suggest growth in the 10–13% range, which may provide some support for

current valuations.

Importantly, our quantitative risk models for both U.S. and international equities remain positive. This has kept us constructively optimistic about equity markets in the short term, despite warning signs from elevated valuations and softening economic data.

Bond Markets and Labor Market Trends

Bond markets also delivered positive returns during the third quarter, as weakening labor data increased the likelihood of a Fed rate cut. Credit spreads on corporate and other non-government debt remain below historical averages and were relatively stable during the quarter—an indication that investors are not yet pricing in an imminent recession.

Two key factors are likely to have a growing impact on financial markets over the coming months and years: (1) ongoing softness in the labor market, and (2) the ballooning federal budget deficit.

Labor Market Developments

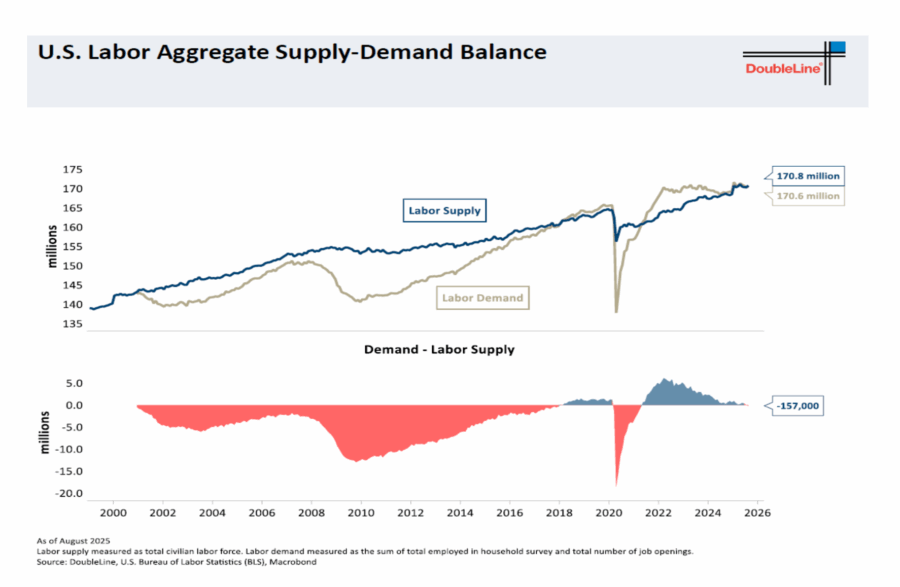

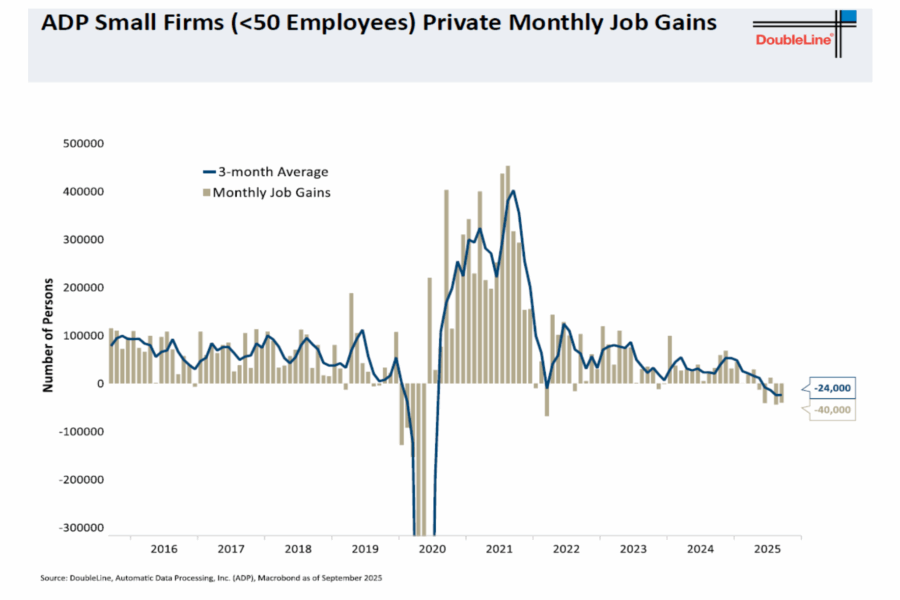

Throughout the year, we’ve seen a consistent decline in job openings and hiring activity. The labor market has moved closer to equilibrium, with a more balanced relationship between job seekers and open positions. However, the trend is clearly weakening. What remains uncertain is the extent to which this softening is due to broader economic deceleration, government budget cuts, or the implementation of AI in the workplace.

Interestingly, the data suggests that small businesses are seeing more pronounced job losses than larger firms. This implies that AI-related job displacement may not yet be a significant factor. That said, labor market weakness—particularly in smaller firms—can still have a meaningful impact on consumer behavior. If workers grow concerned about job security or changing roles, they may delay large purchases like homes and vehicles, both of which are key drivers of economic growth. If current labor trends persist or worsen, the risk of recession will increase meaningfully.

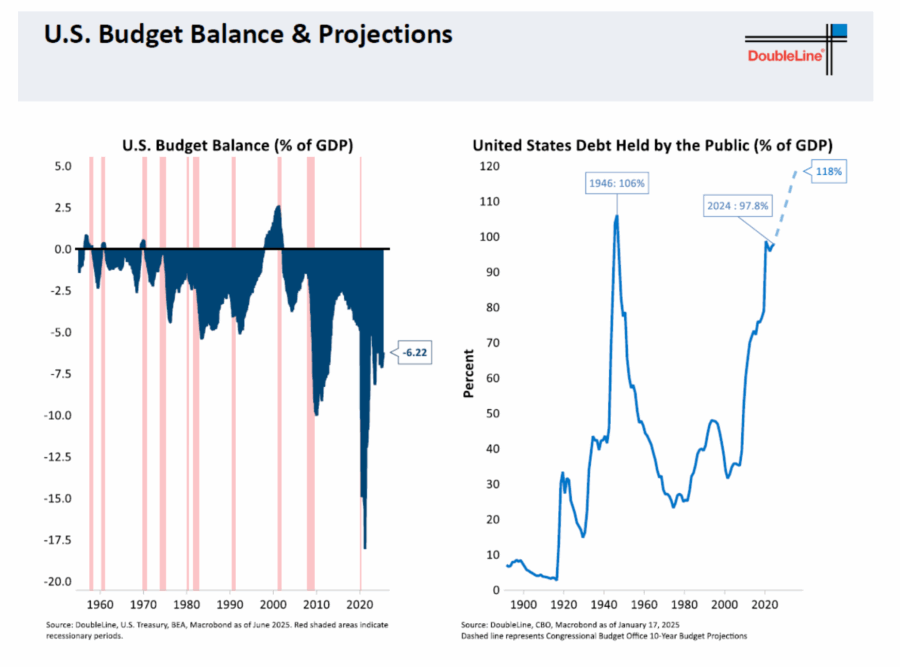

Federal Budget Deficit: A Growing Concern

While we’ve discussed this before, it’s worth highlighting again: the cost of servicing the U.S. national debt has now surpassed $1 trillion over the past 12 months. The chart below shows the scale of the current annual budget deficit and the trajectory of public debt relative to GDP.

Despite the recently passed budget bill keeping tax rates low in the near term, there’s been little progress toward addressing the structural deficit. It appears likely that meaningful reform will be postponed for several more years—yet this challenge will have a growing impact on all of us.

Weatherstone Portfolio Positioning

In terms of portfolio positioning, our models remain positive on both U.S. and international equities. Bond markets are also favorably rated, as continued labor market softness increases the likelihood of one or more additional rate cuts by the Federal Reserve in the months ahead. Overall, we remain constructively positioned for further advances in both stock and bond markets.

We wish you and your family a joyful and restful holiday season. We look forward to providing our next update after the start of the new year.

Warm regards,

Michael Ball, CFP®

Managing Director

Kovitz Investment Group Partners, LLC (“Kovitz”) DBA Weatherstone Capital Management. Weatherstone Capital Management is a division of Kovitz, a registered investment adviser with the Securities and Exchange Commission (SEC). SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete, and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary. The description of products, services, and performance results contained herein is not an offering or a solicitation of any kind. Securities investments are subject to risk and may lose value.