The banking sector is one of the oldest and most important sectors in the makeup of the U.S. economy. Because of this, Weatherstone follows the sector closely to determine whether it should be included in portfolios, and what, if any affect it may have on the broader economy and investment backdrop.

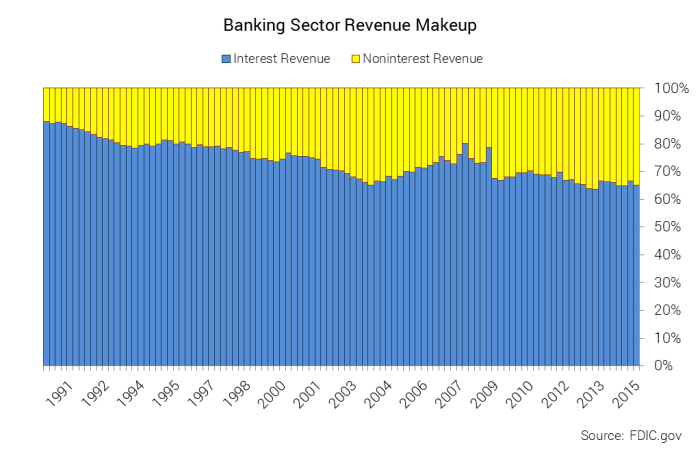

Banks serve two primary functions. First, they serve as a payments system. This system makes it easier for us to make basic transactions among each other and businesses. We deposit money into the bank and can use checks and debit cards to make transactions run smoothly. The second function of a bank is to lend. They take the money we deposit and lend it to individuals and businesses for further business development. Banks make money by charging an interest rate on the loans to those borrowers. Simply put, as long as the rate they are charging borrowers is higher than the rate they pay us for our deposits (e.g. interest you receive on your savings account) they should make money. The higher the difference between the two rates, the more money they make. You can see from the chart below that this interest revenue category has been on a steady decline of a banks overall revenue since the early 1990’s.

Historically, banks have relied almost entirely on interest income as their primary source of revenue. Recently the interest rate and regulatory environment has made it more difficult for the banking sector to turn a profit on lending activities. As a result, banks have shifted even further into noninterest related operations for their source of income. Noninterest income makes up the remainder of a banks revenue and includes income from areas such as:

- Service charges on deposit accounts – examples include overdraft fees, ATM fees, check fees

- Fiduciary Activities – examples include investment management, advisory, and custody services

- Trading account gains and fees –trading securities such as stocks and bonds

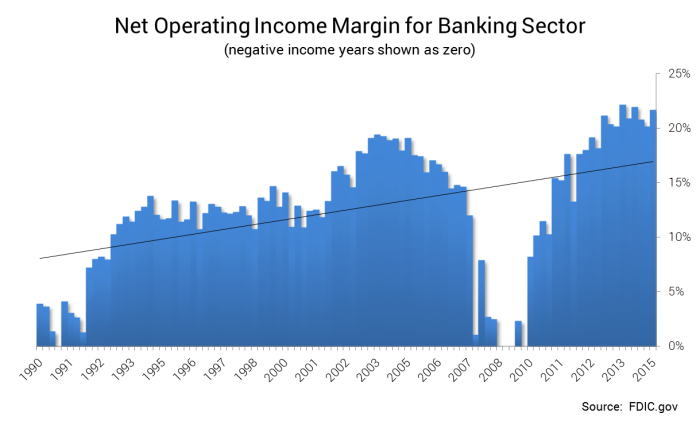

While interest income from lending activities continues to be the primary revenue generator, there is an argument to be made that noninterest income is more profitable and stable and that this revenue generator is being overlooked by investors. Although the trading account gains and fees category may be volatile due to its reliance on how the market behaves and the foresight of the banks’ traders, the revenue generated from service charges and the firms’ wealth management segments should be stable from quarter to quarter. In addition to being more predictable, the noninterest income category appears to be more profitable. The net operating income margin (income less day-to-day operating costs) which is a good indicator for a businesses’ ongoing profitability has been trending higher over the same timeframe as seen in the chart below.

As noted earlier, the banking sector is the primary artery for economic growth. At first glance many would be alarmed by the transformation of the banking sectors’ operational model towards noninterest related income and what it means for the broader economy. The fact is, banks are still lending but they are just diversifying their revenue streams.

Corporate lending has been strong, taking advantage of historically low rates to restructure their capital formation which should set themselves up for a period of positive return on equity. Although many corporations are using some of the cheap capital to repurchase stock, they are also expanding their businesses, evident in the drop in unemployment. We believe this shift in loan growth and corporate capital restructuring will serve as a solid foundation for a fragile economy to lean on.

Current valuations of the financial sector are among the lowest of the ten sectors that make up the S&P 500. Valuation metrics are used as an indicator for the price investors are willing to pay based on their forecast of items such as earnings and sales. With low valuation levels, investors may be signaling that they are still uncertain the path that interest rates will take once the Federal Reserve begins to tighten monetary policy. This uncertainty is justified since interest revenue still accounts for 65% of the banking sector’s revenue (1). However, with more of the banking sector’s income coming from noninterest related services and fees, the level of interest rates should not be as big of a concern as in years past. We will be monitoring the developments and the impact on the finance sector as interest rate change and whether it is a sound investment for managed accounts.

Luke Nagell

Investment Committee

Sources & Disclosure

1. https://www2.fdic.gov/qbp/

Opinions expressed are not meant to provide legal, tax, or other professional advice or recommendations. All information has been prepared solely for informational purposes, and is not an offer to buy or sell, or a solicitation of an offer to buy or sell, any securities or instrument or to participate in any particular trading strategy. Investing involves risk, including the possible loss of principal. All opinions and views constitute our judgment as of the date of writing and are subject to change at any time without notice. The S&P 500 Index is an unmanaged market capitalization weighted price index composed of 500 widely held common stocks listed on the New York Stock Exchange, American Stock Exchange and Over-The-Counter market. Indexes are provided exclusively for comparison purposes only and to provide general information regarding financial markets. This should not be used as a comparison of managed accounts or suitability of investor’s current investment strategies. If the reader has any question regarding suitability or applicability of any specific issue discussed above, he/she is encouraged to consult with their licensed investment professional. The value of the index varies with the aggregate value of the common equity of each of the 500 companies. The S&P 500 cannot be purchased directly by investors. This index represents asset types which are subject to risk, including loss of principal. Investors should consider the investment objectives, risks, charges and expenses of the underlying funds that make up the model portfolios carefully before investing. The ADV Part II document should be read carefully before investing. Please contact a licensed advisor working with Weatherstone to obtain a current copy. If the reader has any question regarding suitability or applicability of any specific issue discussed above, he/she is encouraged to consult with their licensed investment professional. Weatherstone Capital Management is an SEC Registered Investment Advisor with the U.S. Securities and Exchange Commission (SEC) under the Investment Advisers Act of 1940. Weatherstone Capital Management is not affiliated with any broker/dealer, and works with several broker/dealers to distribute its products and services. Past performance does not guarantee future results.