- Last year, U.S. taxpayers paid $360 billion of interest on over $16 trillion in debt, which was the lowest interest expense in seven years.

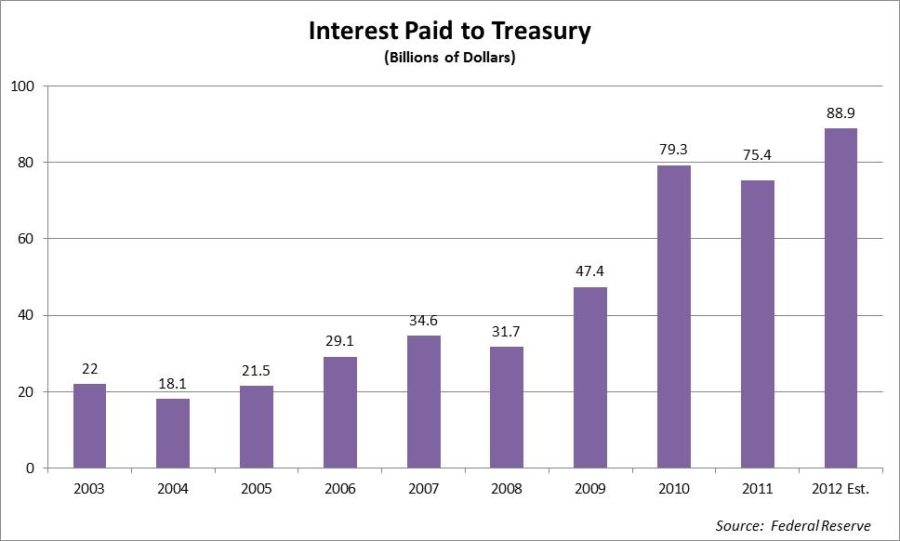

- The Fed paid the Treasury $89 billion last year alone which helped keep the interest expense at such low levels.

- If interest rates take a significant move upward, the Fed will be left with the dilemma of selling its bonds at a loss or holding until maturity.

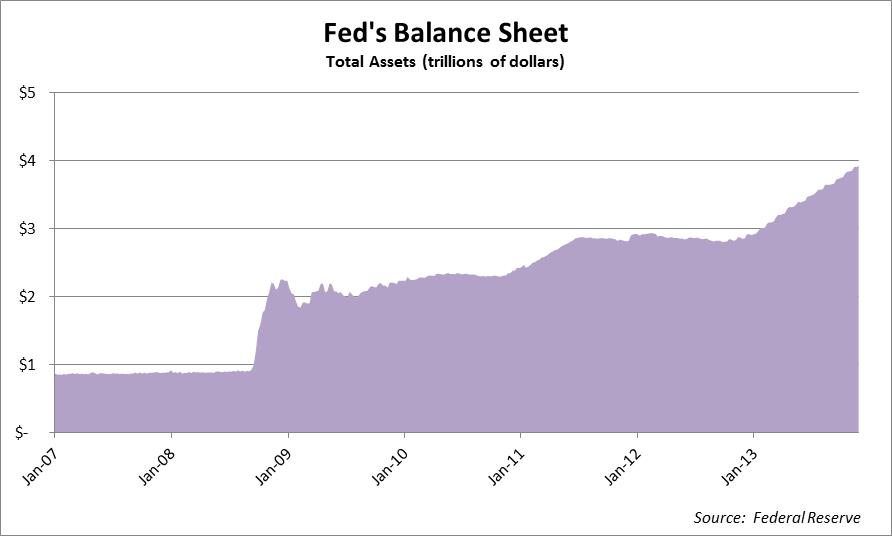

The vast majority of Americans have a hard time wrapping their heads around what the Fed is currently doing and how it affects them. I will try and lay their policies out in a basic and straightforward manner so you can walk away with a good understanding, and provide some good conversation pieces for you to use during the fast approaching holiday season. Basically, the Fed is structured like any other bank in the U.S. with respect to maintaining assets and liabilities and incurring profits and losses. The major asset that the Fed has been building up since the 2008 financial crisis is bonds. By the end of the year, the Fed will have over $3 trillion in treasury bonds and mortgage backed securities on their balance sheet. Just like any other fixed income investor, they hold the assets in their portfolio and receive interest payments on these holdings. What the Fed does with these interest payments has received very little coverage from the financial media and this article should provide some clarity surrounding the Fed’s recent and future activities.

Last year, U.S. taxpayers paid $360 billion of interest on over $16 trillion in debt, which was the lowest interest expense in seven years (1). The Fed is helping the U.S. keep its interest payments low in two different ways. First, the most obvious way is by artificially keeping interest rates at historically low levels. The second and much more obscure way is through its bond purchase program. As I mentioned earlier, the Fed receives interest payments on the roughly $3 trillion in fixed income securities that it holds on its balance sheet. Under law, the Fed must take the income it receives and pay for operating expenses and other expenses such as interest on bank reserves and send the remainder back to the Treasury. The amount that the Fed remits to the Treasury is recorded as a credit towards the interest expense, ultimately lowering the amount that taxpayers have to pay.

As you can see from the chart below, this remittance to the Treasury has grown significantly over the past few years as the amount of bonds it holds has increased. The payment last year alone was more than the $85 billion in budget cuts, famously dubbed sequestration.

Although this may seem like a great scheme to finance a portion of our debt at 0% interest rates and lower our government spending, the party won’t last forever. Just like any other holder of fixed income securities, if and when interest rates begin to rise, the Fed will incur losses on their bond holdings if they sell them prior to maturity (bond prices and interest rates move inversely). These losses could be problematic for the Fed and for policy makers if rates were to take a significant move upward. If the Fed were to incur these losses, it would be a loss on its income statement and depending on the increase in interest rates could supersede any income received in interest on its holdings. As a result, the Fed’s payments to the treasury and consequently tax break to the U.S. taxpayer would disappear.

Statement from the audit of the Fed’s financial statements: “If earnings during the year are not sufficient to provide for the costs of operations, payment of dividends, and equating surplus and capital paid-in, remittances to the Treasury are suspended. A deferred asset is recorded that represents the amount of net earnings a Reserve Bank will need to realize before remittances to the Treasury resume. This deferred asset is periodically reviewed for impairment.” (2)

Although the budget cuts were more painful than losing taxpayer provided entertainment like flyovers at sporting events, the pain could have been much worse if the Fed did not partake in some of its monetary policies. Furthermore, the pain could get much worse if some of the worst case scenarios play out down the road. The bipartisan Congressional Budget Office (CBO) releases a budget projection every year for tax revenues and government spending and provides a roadmap for the next 20 years. Within the most recent report, the CBO projected that interest expense will surpass defense spending for the first time in history by the year 2021. This projection was based on a 10-year treasury yield rising gradually to 5% by 2017 and staying constant at 5.2% from 2018 until 2023(3). The interest rate projection provided by the CBO is a base case scenario but there is always the possibility of significantly higher interest rates as a result of runaway inflation or investors dumping U.S. debt securities.

Over the past year, fixed income portfolio managers have been lowering the duration of their portfolios by shifting to floating rate instruments, short term securities and cash. These professional money managers have been making these adjustments to safeguard their portfolio from large capital losses as a result of a rise in interest rates. At the same time, the Fed has been extending the duration of its fixed income portfolio by purchasing longer term treasuries and mortgage-backed securities (4). This creates a big challenge for the Fed since the size of the loss that a fixed income portfolio incurs from rising rates, otherwise known as interest rate risk, is positively correlated to the duration of its portfolio (i.e. the longer the duration, the greater the interest rate risk).

Over the course of 2013, Weatherstone has also been making adjustments to its fixed income portfolios during the current dynamic interest rate environment. In addition, we are keeping a watchful eye on the conundrum outlined above that could create headwinds or tailwinds for economic growth. For example, if interest rates take a significant move upward and the Fed begins to sell its holdings at a loss, they would no longer be able to provide income remittance to the Treasury which would create further challenges for policy makers when making budget decisions and ultimately creating headwinds for economic growth. However, if the Fed decides to hold their bonds until maturity to avoid realizing any losses or if interest rates remain at suppressed levels, all else equal, tailwinds for economic growth could continue for the foreseeable future. As the events begin to unfold we will be adjusting our equity and fixed income portfolios accordingly.

Happy Holidays!

Luke Nagell

Investment Committee Member

Sources:

(1) http://www.bloomberg.com/news/2012-10-04/u-s-interest-cost-falls-to-lowest-since-2005-as-debt-soars-1-.html

(2) http://www.federalreserve.gov/monetarypolicy/files/BSTcombinedfinstmt2012.pdf

(3) CBO.gov

(4) http://blogs.wsj.com/economics/2013/02/06/u-s-treasury-considers-ways-to-extend-debt-maturity/

Disclosure: Opinions expressed are not meant to provide legal, tax, or other professional advice or recommendations. All information has been prepared solely for informational purposes, and is not an offer to buy or sell, or a solicitation of an offer to buy or sell, any securities or instrument or to participate in any particular trading strategy. Investing involves risk, including the possible loss of principal. All opinions and views constitute our judgment as of the date of writing and are subject to change at any time without notice. Investors should consider the investment objectives, risks, charges and expenses of the underlying funds that make up the model portfolios carefully before investing. The ADV Part II document should be read carefully before investing. Please contact a licensed advisor working with Weatherstone to obtain a current copy. Weatherstone Capital Management is an SEC Registered Investment Advisor with the U.S. Securities and Exchange Commission (SEC) under the Investment Advisers Act of 1940. Weatherstone Capital Management is not affiliated with any broker/dealer, and works with several broker/dealers to distribute its products and services. Past performance does not guarantee future results.